EDITOR’S NOTE: To read this article in its entirety, visit the digital edition of the April issue by clicking here.

If it seems like the pace of mergers and acquisitions in the RV industry is accelerating, you’re not imagining it.

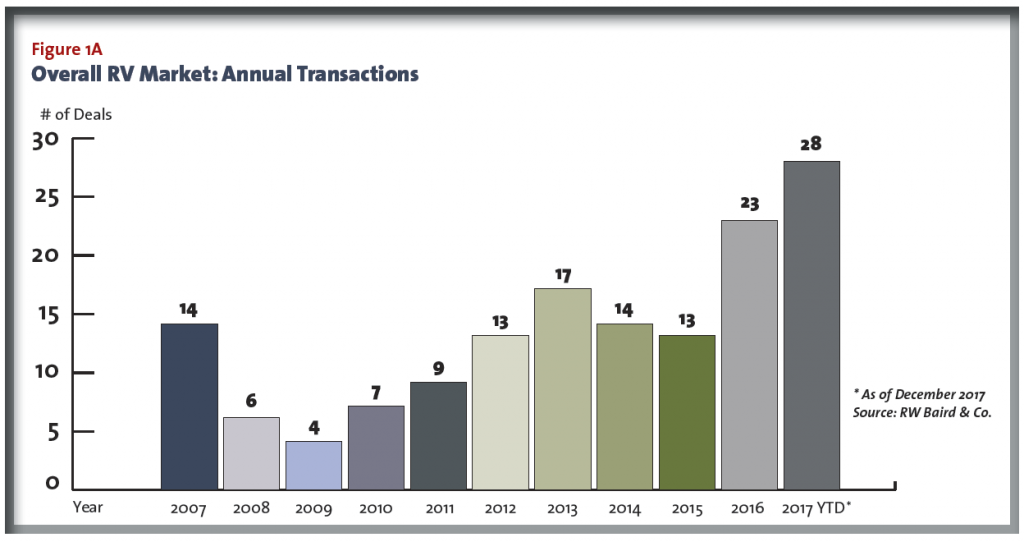

During the past two years, the number of these transactions totaled at least 45, up from 27 in the previous two years and well ahead of any two-year period since the Great Recession, according to investment banking firm Baird & Co., which tracks publicly available data. Baird says that, since 2007, RV-related firms have announced at least 138 transactions.

“Overall RV market M&A activity has returned to pre-recession levels with a meaningful uptick in 2016 and 2017 year-to-date,” according to Baird data, which was generated late in 2017.

Figure 1A

There are several reasons for this uptick. M&A activity for all U.S. businesses has been steadily climbing since the low point of the Great Recession. Fueling this robust trend in particular for the RV industry have been strong consumer demand, low interest rates, significant capital availability and strong balance sheets, according to Eric Stetler, director of Baird’s Global Banking Investment Group.

While Baird does not assign a specific aggregate value of the M&A transactions it counted, Stetler says, “For transaction volume, we currently have $4 billion-plus that is disclosed. Our specific knowledge of larger, non-public deals confidently gets us to $5 billion-plus. I think we can probably say at least $6 billion-plus.”

Baird’s data of M&A activity shows deal-making across major segments, including:

- RV Makers: Baird tracked 30 transactions during the 11-year study period, driven by players including Thor Industries, which has alone acquired five companies during this period to solidify its position as the No. 1 RV manufacturer, and REV Group, which has acquired Lance Camper, Midwest Automotive Designs and Renegade RV in just the past two years. Meanwhile, a number of smaller acquisitions also have taken place, such as Chinook RV’s acquisition of Vohne Liche Mfg. (formerly Riverside Travel Trailer) in early 2018. Baird says benefits of such deals include greater market penetration and more purchasing strength.

- Suppliers. Baird recorded 80 transactions during the 11-year period, with a high of 13 in 2017. Large RV suppliers such as Patrick Industries, Lippert Components, Dometic Corp. and Airxcel have driven much of the consolidation. Baird anticipates consolidation will continue, given benefits of scale and synergies realized.

- Dealer/Distributors. Baird recorded 58 transactions over the 11-year period, with a high of 14 reported through Nov. 30, 2017. Camping World completed at least 10 dealer acquisitions in 2017 alone. Baird expects transaction volume to increase further as small, privately held dealers sell to larger players. Meanwhile, there has been a seismic shift in the distributor market with LKQ/ Keystone’s acquisition of national players NTP, Stag-Parkway and Coast Distribution.

Notably, Baird limited its analysis to RV manufacturing, supply or distribution, so a number of transactions involving RV-related businesses were deliberately not counted. For example, Forest River’s purchase of bus manufacturer Turtle Top, Patrick Industries’ acquisition of logistics firm Indiana Transport and Brown & Brown’s purchase of MBA Insurance. Another aspect of the RV industry – campgrounds and RV parks – also does not figure into Baird’s data, even though this end use for many RVers has been an active investment target in 2017.

With so much consolidation in the industry over the past decade, “few substantial OEM deals remain to be made,” Stetler says. The key word is “substantial,” given that all of the 70-some vehicle OEMs and 30-some park model manufacturers that remain independently owned would be considered “small” compared to the 2016 blockbuster deals, such as Thor Industries acquisition of Jayco for $576 million and Winnebago Industries purchase of Grand Design RV for $520 million.

Stetler adds, “We see another strong year in 2018 for overall transaction activity supported by modest organic growth, a continued low interest rate environment and significant available cash/liquidity both on corporate balance sheets and with private equity. Tax reform is another catalyst to earnings and deal making.”

A quick glance at top industry news headlines during the past four months would seem to support Stetler’s contention, with REV Group buying Lance Camper, Lippert purchasing Hehr’s window and glass business, and Camping World acquiring several outdoor gear and apparel businesses.

Stetler says M&A activity thrives in good times – and these are certainly good times. The RV industry grew like gangbusters in 2017, with RV wholesale shipments pegged at 504,599 units, up from 17 percent from the 430,691 units shipped in 2016. For 2018, RVIA is forecasting shipments will reach 520,700 units.

M&A Activity Brisk in Northern Indiana

Baird’s investment bankers have been working behind the scenes on some of the major M&A transactions in the RV industry in the past decade. Notable deals include the sale of Coachmen RV to Forest River in 2008, all of the public stock offerings by Camping World Holdings and REV Group, the sale of Atwood Mobile Products to Dometic Corp., the sale of Grand Design RV to Winnebago Industries and the recently announced sales of Airxcel to LCatterton.

This activity underscores how closely Baird works with the RV industry. And with an estimated 80 percent of RVs manufactured in Indiana – where many suppliers are also located – that’s where many of the buyers and sellers also are located.

“We travel around Indiana quite a bit,” Stetler says.

So does the team at Legacy Capital Advisors, a Chicago-based M&A boutique, which exclusively provides sell-side M&A advisory services to closely held, middle-market companies. Since its formation in 2001, Legacy has provided its clients with more than $2 billion of liquidity. RV and related industry clients have included B&B Molders, Big Tex Trailers, Cana Cabinetry, Foremost Fabricators, Noble Composites, North American Forest Products, Quality Hardwoods and Wells Cargo.

Managing Director Kevin Keuper says, “Four of the five partners at Legacy Capital, as well as two of our advisory board members, have recently been in Northern Indiana working on deals. M&A activity has been quite active.” (Keuper was interviewed for this story in November.)

When asked what constitutes a good deal, Keuper says, “When the seller receives a very good price, great terms and a great home for the management and employees, while the acquirer derives synergistic value in the acquisition, it’s a good deal.”

Sellers sometimes stay on after the sale to ease the transition; sometimes they leave immediately. Sellers are typically required to sign non-compete contracts reaching out four or five years.

A third player behind the scenes is Mark Sage, an investment banker and managing director of Tampa-based Wyndham Capital, who has worked as a mergers and acquisitions consultant back to 1979. Since 2013, his firm has represented three RV manufacturers as well as five modular/HUD manufacturing firms that were sold.

“We’re in discussion with two manufacturers and a retail dealership who are interested in selling. It’s a matter of timing, waiting for end of year numbers to come up,” Sage told RV PRO in late 2017.

Key Drivers in RV M&A

Compared to other sectors covered by Baird’s consumer and industrial groups, “RV has experienced generally more OEM consolidation and increasing activity in the supply chain and distribution over the past few years,” Stetler says. “The centralized nature of the industry has been a likely key factor.”

Stetler and Mike Lindemann, managing director of Baird’s Global Investment Banking Group, say several key themes emerge from a closer look at the M&A activity:

- Private equity: An extensive search of public records by RV PRO found more than 50 transactions involving private equity (PE) firms as either buyers or sellers during the past 27 years. PE investment in the RV industry spans the width and breadth of the market – including manufacturers, suppliers, distributors and dealerships. Notable PE investors over the years have included LCatterton Partners (Heartland RV), Industrial Opportunity Partners (Roadtrek), Linsalata Capital Partners (Stag-Parkway), The Sterling Group (Dexter Axle), Audax Group (CURT Group), One Rock Capital (Airxcel), Summit Partners (Grand Design RV), Wayzata Investment Partners (Lazydays RV) and Crestview Partners (Camping World). The PE player perhaps making the largest impact in the RV sector is American Industrial Partners (AIP), which created REV Group, which now encompasses the iconic RV brands Fleetwood, Monaco, Holiday Rambler, Renegade RV, Midwest Automotive Design and, most recently, Lance Camper.

- Diversification: Lippert Components has broadly expanded into other types of components and entered new end markets, as exemplified by its January purchase of Marine supplier Taylor Made Group and its 2017 acquisition of European RV suppliers Metallarte and Sessa Klein. Separately, Patrick Industries continues to diversify with the acquisition of three marine businesses in mid-2017. And in perhaps the biggest and best example of diversification, Camping World has purchased several camping gear and outdoor lifestyle companies, including Gander Mountain, Overton’s and Erehwon Mountain Outfitter. For its part, Winnebago says by the year 2020, 10 percent of its revenue will come from RV segments or businesses it isn’t in today.

- International ties: At the same time American RV businesses have been acquiring RV and marine companies outside of the United States to expand their markets, European companies are buying RV businesses in North America, attracted by its large market and favorable business climate. Two of the best examples of this trend are German RV maker Erwin Hymer Group, which purchased Canada-based Roadtrek in 2016, and Swedish supplier Dometic, which bought U.S.-based supplier Atwood Mobile Products in 2016.

As merger and acquisition activity has intensified in recent years, many have questioned what it means for the future of the industry, and some have lamented the loss of mom-and-pop businesses to larger, more corporate companies. For their part, though, the Baird bankers see consolidation as positive on the whole.

“OEM and dealer consolidation, as well as better management of consumer and trade credit and inventory at all levels of the RV value chain, have improved the industry and created an environment for sustainable growth,” Stetler says. “OEM and supplier consolidation generally creates larger, more financially sound companies and enables deeper, more balanced relationships.”